Institutional Proof of Reserves: How Verifiable Transparency Unlocks Better Lending Terms

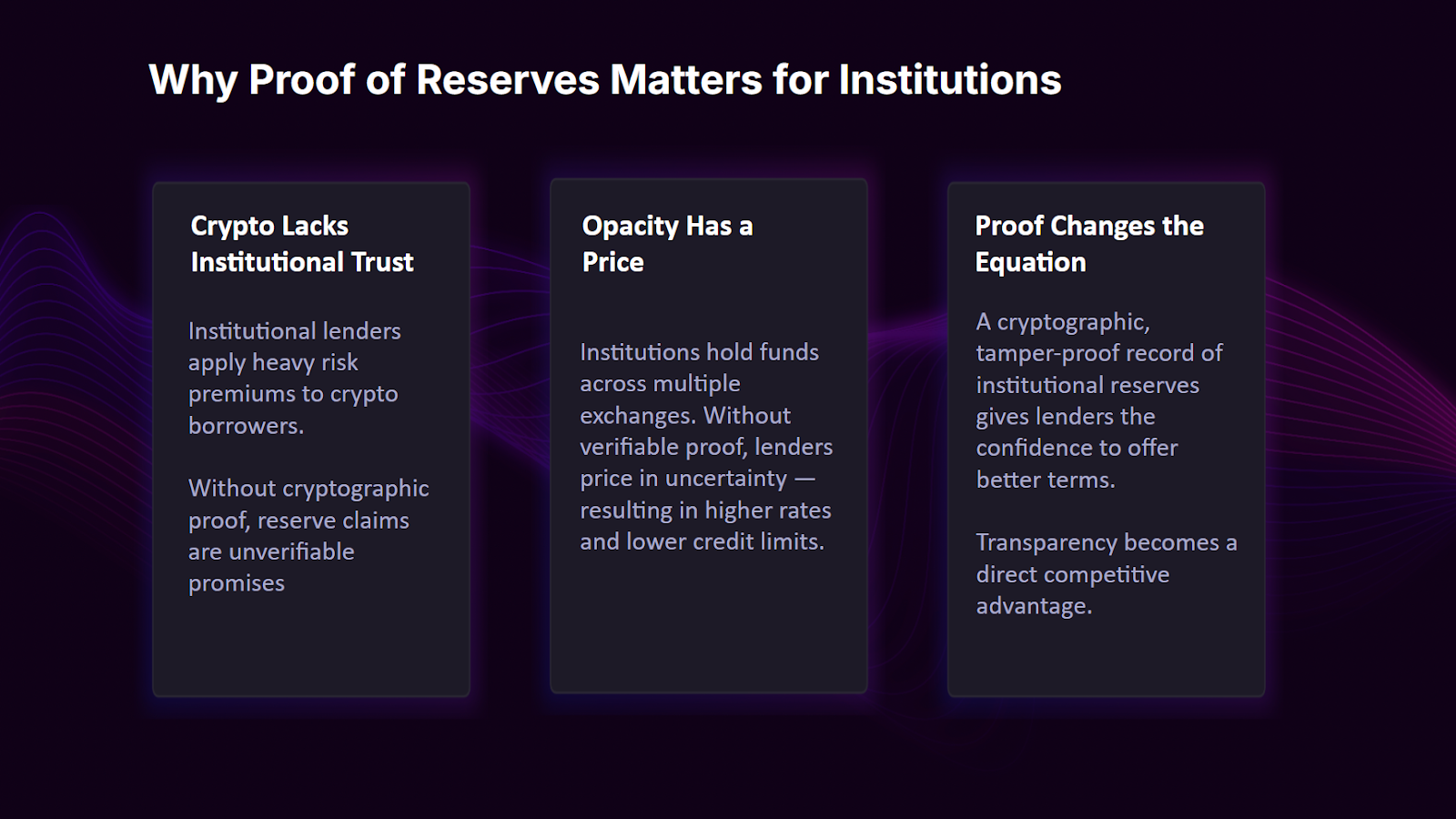

Every crypto institution that borrows knows the feeling: you're sitting on substantial reserves across multiple exchanges, but your lender treats you like a black box. The interest rate reflects not your actual risk profile, but the lender's inability to verify your claims. You're paying a premium due to opacity, and it can be an expensive one.

This is the core problem that institutional Proof of Reserves solves: not transparency for its own sake, but transparency as a financial instrument, one that directly reduces the cost of capital for firms that can prove what they hold.

The Trust Premium in Crypto Lending

Institutional lending in crypto currently operates under a structural disadvantage compared to traditional finance. When a corporation seeks a loan in traditional markets, the lender can review audited financial statements, examine regulatory filings, and rely on established frameworks for assessing creditworthiness. Though some information asymmetry still exists, it’s managed through decades of infrastructure.

In crypto, that infrastructure doesn't exist in the same way. A trading firm might hold hundreds of millions of dollars across Binance, Coinbase, Kraken, and a half-dozen other exchanges, but proving that to a lender means sharing screenshots, API exports, or periodic reports, all of which can be fabricated, are stale the moment they're generated, and none of which provide guarantees about what happens between reporting periods.

Lenders know this. They price loans accordingly.

The result is what could be deemed an "opacity premium," the additional cost that borrowers pay because lenders can't independently verify reserve claims. This manifests as higher interest rates, lower loan-to-value ratios, larger collateral requirements, and stricter borrowing conditions. For well-capitalized firms, it's a frustrating tax on opacity rather than on actual risk.

Why Traditional Audits Don't Cut It

The obvious response is: get an audit. And many institutional players do engage auditing firms to verify their holdings. But traditional audit approaches have significant limitations in the crypto context.

First, audits are periodic. Even quarterly attestations leave 90-day gaps in which a firm's reserve position could change dramatically. In crypto markets, where positions can shift by double-digit percentages in a day, a three-month-old audit carries limited weight and could be almost entirely without value in certain situations.

Second, audits are entirely backward-looking. They tell a lender what was true at a past date, not what's true today. A firm that passed an audit in January could be in a fundamentally different position by March, and the lender would have no way of knowing the facts until the next attestation.

Finally, audits depend on auditor credibility. In the wake of several high-profile collapses – notably FTX, Celsius, and Voyager – questions about the competence and independence of some crypto-focused auditing firms became legitimate concerns. When Mazars paused its crypto audit work in late 2022 – over concerns about the limitations of Proof of Reserves reporting, no less – it highlighted how thin the bench of qualified and trustworthy crypto auditors really is.

For institutional borrowers, the implication is clear: traditional audits are necessary but inadequate. They don't give lenders the confidence to meaningfully improve terms, because the gaps between audits remain a source of unquantifiable risk.

What Lenders Actually Need

When you strip away the jargon, institutional lenders want answers to a set of questions. And they require that those answers be fully trustworthy.

"What do you hold right now?" Not last quarter. Right now. Lenders want near-real-time visibility into a borrower's reserve position, or at minimum, daily attestation that balances haven't materially changed.

"Can I verify this independently?" Self-reported data isn't enough, no matter how detailed, because it can be manipulated. Lenders want the ability to check claims against an independent source.

"Is this the complete picture?" Reserves spread across 10 exchanges are only meaningful if the lender can see all 10 accounts. Partial visibility creates much the same uncertainty as no visibility. The question just shifts from "do they have reserves?" to "what are they hiding on the other exchanges?"

"Can I trust the math?" When a borrower reports a total reserve figure, the lender wants confidence that the aggregation was done correctly: that no balances were double-counted, no accounts were omitted, and the computation itself hasn't been tampered with.

A system that answers all four of these questions with cryptographic certainty rather than institutional trust fundamentally changes the risk equation for lenders, and therefore the terms that they’re willing to provide.

How Trustless PoR Changes the Economics

Consider a crypto trading firm that borrows $50 million against its exchange reserves. Under current conditions, a lender might charge 12-15% annualized, reflecting the uncertainty around the firm's actual reserve position. Though the firm is well-capitalized, it can't prove that in a way the lender finds sufficiently convincing.

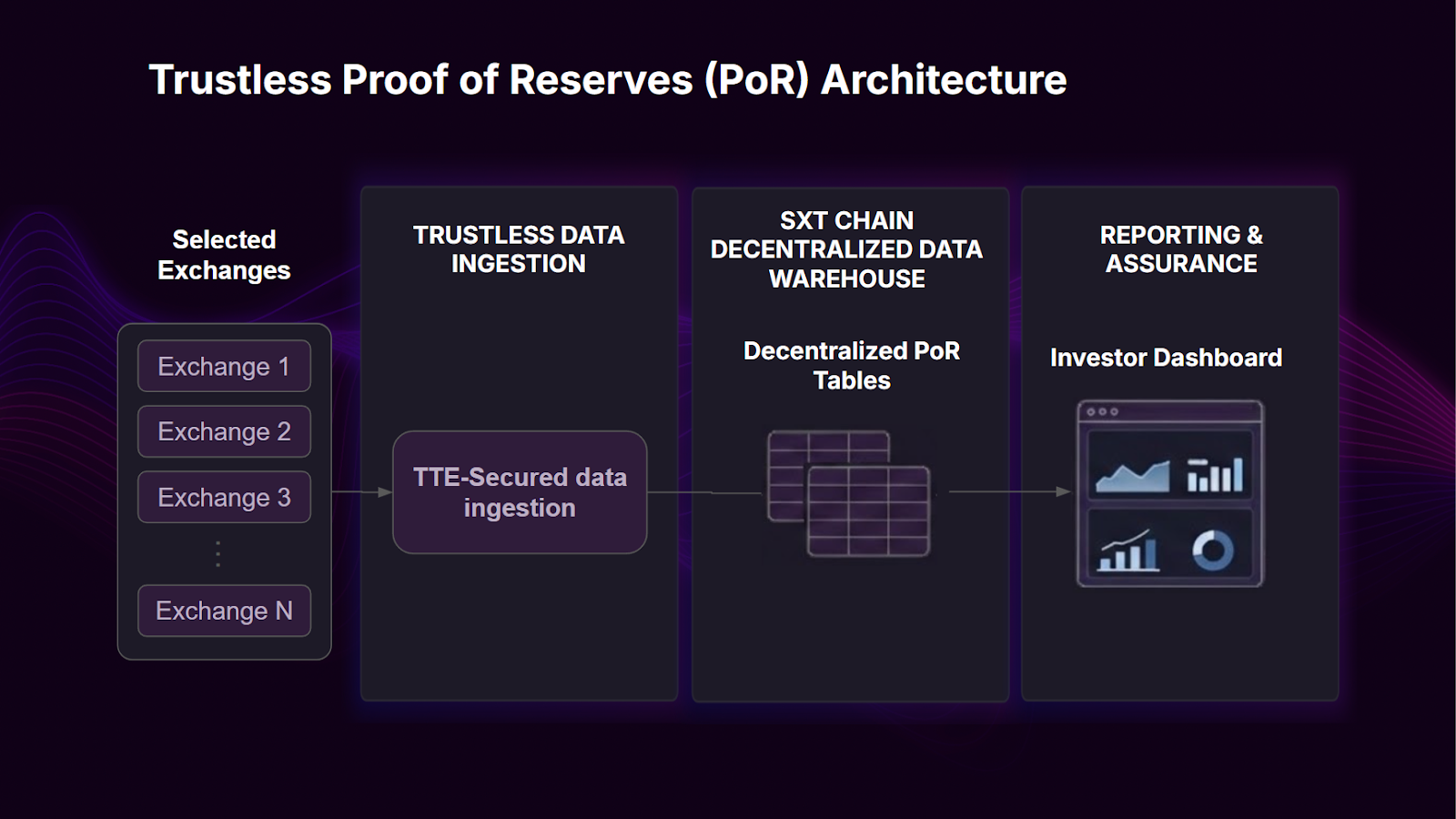

Now imagine that the same firm implements a trustless Proof of Reserves pipeline. Its balances across every exchange are fetched daily through hardware-attested connections, indexed into a decentralized database, and made queryable with cryptographic verification. (For a full walkthrough of how this architecture works, see our deep dive on trustless Proof of Reserves.) When the lender runs a coverage ratio query, the result comes with a Proof of SQL verification: mathematical certainty that the computation was run faithfully against untampered data.

The lender's risk calculus changes. The “opacity premium” disappears. The firm isn't asking the lender to trust a report; instead, it's giving the lender the ability to verify the firm’s reserves for itself, continuously, with cryptographic guarantees.

The rate drops. The credit limit increases. Collateral requirements soften. Not because the firm's actual financial position changed, but because the lender can see that position with confidence.

For a large loan agreement, even a modest improvement in lending terms for an institution can add up to a large savings. At that scale, the cost of implementing a PoR pipeline can pay for itself within the first year.

The Multi-Exchange Challenge

The lending angle becomes especially compelling for firms that operate across many exchanges, which is to say, most institutional crypto players.

A market maker providing liquidity on 10 or 20 exchanges doesn't have a single balance to prove. It has a fragmented reserve position spread across platforms with different APIs, different reporting formats, and different levels of cooperation. Aggregating all of that into a single, verifiable reserve picture is precisely the sort of problem that traditional PoR approaches can't solve.

A trustless pipeline handles this natively. Each exchange integration follows the same pattern and feeds into a single, unified database. Whether it's three exchanges or fourteen, the architecture is the same. The view just gets more complete.

From the lender's perspective, this is transformative. Instead of evaluating fragments of information from different sources in different formats on different schedules, they get a single dashboard showing the firm's total reserve position, updated daily, queryable in real time, and verifiable with Proof of SQL. The "complete picture" problem is solved by design, with the accompanying improvements to lending terms.

Balancing Transparency With Competitive Sensitivity

A legitimate concern for institutional players is that full reserve transparency could reveal competitive information. A market maker's balances on specific exchanges can indicate its trading strategy, market focus, and relative activity levels. Broadcasting that data publicly could be commercially damaging.

Trustless PoR systems address this through granular data privacy. Individual balance data points can be encrypted at the ingestion layer, making the raw data invisible to anyone without authorization. Lenders and approved counterparties would access a private dashboard where the data is decrypted for their view. Everyone else would see that attested, verified data exists, but would be unable to access any of the details.

Proof of SQL makes this privacy practical rather than theoretical. Authorized lenders who query the data receive results that are cryptographically proven to be correct computations over untampered data. The verification isn't about trusting the dashboard or the data operator; it requires only trusting the math. Meanwhile, unauthorized parties can't access the underlying data at all, because encryption controls who sees what.

This means privacy is additive. It layers on top of the verification architecture rather than replacing it. The data remains verifiable and immutable onchain, but access to the details is controlled.

What Implementation Looks Like

For an institution considering a trustless PoR deployment, the practical path is more straightforward than the technology might suggest. Space and Time has built the end-to-end infrastructure: from trustless data ingestion through TEE-secured connections, to indexing in SXT Chain's decentralized database, to a lender-facing dashboard with Proof of SQL verification. The architecture scales across an institution's full exchange footprint, producing a single, continuously verified picture of total reserves without the institution needing to build or operate the underlying infrastructure itself (and therefore also open up the potential for the institution to tamper with that infrastructure).

The Competitive Edge

In a market where every crypto institution is competing for capital on similar terms, verifiable reserve transparency can be a genuine differentiator. The firm that can show a lender exactly what it holds, with continuous updates, independent verifiability, and mathematical proof of correctness, gets the loan on better terms than the firm that offers a quarterly, tamperable PDF report.

As the institutional crypto market matures, this dynamic will only intensify. Lenders will increasingly expect verifiable reserves as a baseline rather than as a differentiator. The firms that implement it now will gain an early-mover advantage in lending relationships. The firms that wait will inevitably face it as a requirement down the line.

The infrastructure exists today. SXT Chain provides the decentralized database and Proof of SQL verification layer. TEE-secured data ingestion solves the trustless collection problem. Encryption and access controls handle privacy where needed.

The question isn't whether trustless PoR will become standard for institutional crypto lending. It's which firms will adopt it first and capture the advantage while it's still a differentiator.

Make your reserves continuously verifiable with trustless Proof of Reserves here